Why Invest in European Venture Capital Funds?

European startup scene has been increasingly well documented in the recent years thanks to Atomico’s excellent State of European Tech report, which we’ll also utilize here, but what does that mean for returns to Limited Partners from European Venture Capital funds, both looking backwards in history and forwards to the future? We aim to find out below.

According to Europe’s most prominent VC fund investor, European Investment Fund (EIF), capital efficiency of VC-backed companies exiting at USD1Bn or above in ICT (Information and Communication Technology) sector is highest in Europe globally - returning 5.5x invested capital compared to 5x in USA and 4x in Asia.

On fund performance level, for the most recent vintage available, according to EIF the top half of all European VC funds delivered IRR of 5% or above, with the top quarter delivering a range from 25% to 371% annually.

There are now 118 funds delivering positive returns in Europe. And those 118 funds represent a large percentage of what is available in the market: even third quartile funds in ICT produce 8.17% IRR rates (Life science is close behind at 7.40%. Growth funds produce 8.05%) And even the bottom quartile losses are limited to 1.05% per year.

How does the average European VC fund compare to the US?

It is very difficult to make these comparisons: the data has to lag quite a lot in order to smooth out irregular events in the first immature years of the fund. Also the indices globally have very different compositions: if America has more late stage funds in general than Europe, then performance can be expected to come through earlier and outperform. For example, the European index may contain many more low-quality funds, as EIF that invests in a large percentage of the commercially viable composites of that index regularly outperforms it. But for comparison’s sake, the index is provided in both regions, not the selection of the index that EIF represents. That said, the below can still offer an illustration of the fact that contrary to the popular opinion, Europe does not always lag behind US and even in the year that it does, the absolute level of return is still quite high. Note that two of the instances of outperformance happened in the latter half of the measurement period, displaying an upwards trend (unfortunately tempered by the underperformance of 2015)

Source: EIF

European VC now also compares favourably to liquid asset classes: over the last 10 years of available data period (2006 to 2016), EIF’s portfolio has beaten the STOXX index in Europe 8 times out of 10, whereas in the previous decade, the ratio was reversed. The same is true for other geographies, where EIF’s portfolio also beat S&P500 eight times out of ten.

REALISED RETURNS

Europe has raised considerably less capital than US, both for start-ups as well as for funds, although the trends on both sides are changing. 2020 saw record levels of investment into European VC funds at $7.8Bn in the first half of the year (including unprecedented megafunds from Atomico at $820m and Index Ventures at $800m). According to Ben Evans, capital invested in European start-ups has quadrupled over the last decade (EUR41bn in 2020 according to Dealroom.co) and is now at 15% of that invested in California, which may well prove to be a tipping point to fully catalyse the ecosystem. But more importantly, in addition to the European companies being 5.5x more capital efficient as mentioned above, also at fund level Europe does 2.5x better than USA with the capital it does raise in terms of producing and exiting Billion-dollar-plus companies:

The billion-dollar-plus exits and the new era of maturity for European VC were kicked off by Skype from Estonia that was sold to eBay in 2005 for EUR2.2Bn. Skype was founded in 2002 and raised c. $2m Seed/Series A in in 2003, estimated to have returned 350x capital (estimated entry value c. $5m) and a $19m Series B in 2004 (Bessemer, Index, Mangrove) that is estimated to have returned 40x capital (estimated entry value c. $67m). Skype reached 100m registered users in 2006, $382m revenues in 2007, $1bn in 2009. Skype founders went on to become VCs and serial entrepreneurs. Other notable acquisitions in European tech market history have been Supercell for EUR 9.2Bn and Skyscanner for EUR 1.5Bn

21% of those unicorns founded in the 2010s have been acquired, with the largest M&A transaction of the decade currently being PayPal’s 2018 $2.2bn acquisition of iZettle. iZettle’s last round before the exit was valued at $950m less than a year earlier, creating 2.3x return in c. 10 months, which translates to close to 100% IRR. Its series D a few years earlier was EUR 500m, generating 4x returns to fairly late stage investors in three years. The earlier Series A and Series B valuations are not publicly disclosed, but the returns are likely to be in double digits.

In addition to full acquisitions, many European unicorns like Transferwise and Klarna have also had significant secondary rounds, at $5Bn and $11Bn valuations respectively, creating liquidity at high returns for early investors. UIPath is also expected to have allowed secondary sales at $8Bn valuation

35% of those unicorns founded in the 2010s have IPOed. Since 2016, Europe has had more tech IPOs than USA annually, 36 in 2020. Most remarkably, Spotify IPOed at $24Bn valuation. Unity, which does not even get counted as a European startup as it’s headquartered in San Francisco, but has Danish founders nevertheless, IPOed at $16Bn in 2020. In 2014 Just Eat IPOd for EUR2bn, Zalando for EUR5.3Bn, in 2017 Delivery Hero for EUR4.4Bn. Farfetch for 5.2bn.

YET TO BE REALISED:

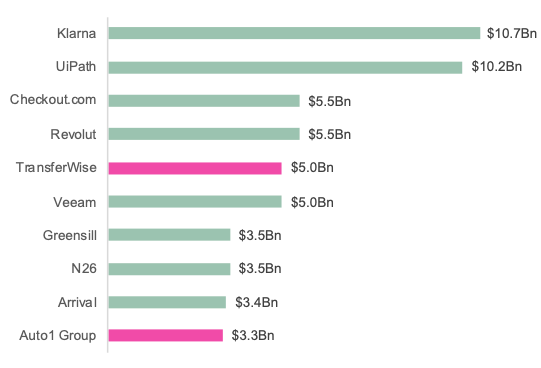

These are currently the ten highest valued privately held VC-backed tech companies in Europe. Of these, Auto1 and Transferwise are expected to IPO immediately.

WHAT IS DRIVING THESE RETURNS?

EUROPE AS A MARKET AND A TECH ECOSYSTEM:

In 2019, the EU28’s GDP stood at ca. USD 18.4t, the United States’ GDP at USD 21.4t, and China’s GDP at USD 14.3t. While the United Kingdom is leaving the EU, it is not leaving the continent, so still counts as a home market even under a different legislative regime. Europe’s tech industry is growing 5X faster than the rest of the economy.

The EU is the #1 exporter globally. Extra-EU27 trade surplus was USD 217.6b, while the United States produced a trade deficit of USD 616.8bn and China reported a trade surplus of USD 106.6b. The European national markets are too small to establish and sustain global companies on home markets alone, which is why European companies internationalize from day 1 - first within Europe and then globally. And technology companies with their digital products and virtual distribution channels are able to take the best advantage of it.

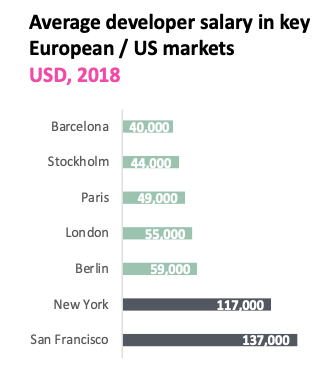

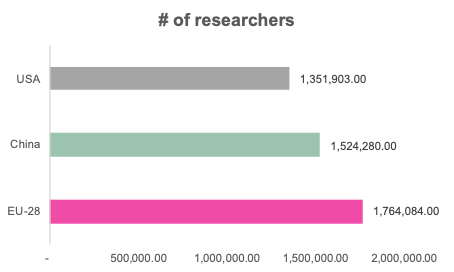

Europe has ca. 5.5m software developers (vs. 4.2m in the United States), The continent also has the most fulltime researchers globally, ahead of China and the United States and it’s home to 5 of the top 10 computer science universities globally. And in 2019, the EU had more than 850k STEM graduates, while The U.S had ca. 600k according to Atomico’s State of European Tech Report 2019

Europe is a market of similar population, economic output and mobile penetration to the US, and has more developers per capita. Yet, it sees just $45 per capita in venture capital investment, compared to $304 in the US.

PARTS OF EUROPE ARE EVEN MORE UNDERSERVED

THAN OTHERS:

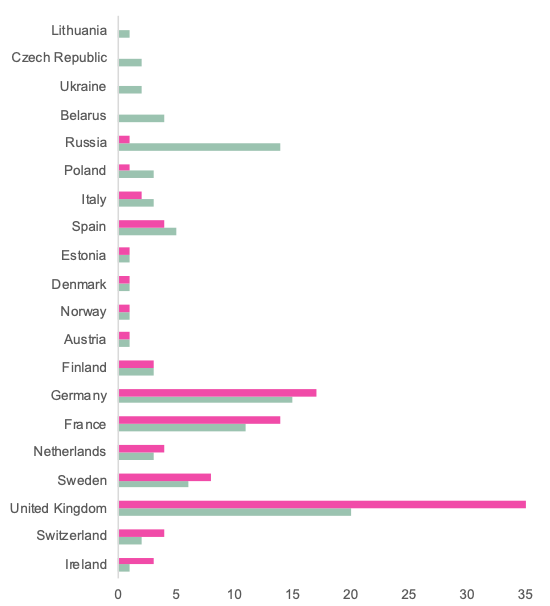

The companies which raised megarounds in 2020 came from all corners of the continent — Sweden’s Klarna ($650m) and Northvolt ($600m), the UK’s Revolut ($580m), Karma Kitchen ($317m) and Cazoo ($310m), Germany’s Auto1 Group ($300m), Lilium ($275m) and Tier ($250m), France’s Mirakl ($300m) and Romania’s UiPath ($225m). But there’s high potential in even more remote corners than that, as many of the countries away from hubs are producing outsized numbers in terms of companies with over $1m of consumer spend compared to the amount of capital invested in the country Particularly, Baltics and Eastern Europe are worth taking a look at, whereas Western Europe may already be overinvested:§ Share of capital invested 2016-2020

All of the above indicates the opportunity in Europe is very much there and in some cases exceeding the US.

Write first comment